In recent years, mini-games have emerged as a major force, quickly becoming a key focus of the domestic gaming industry. The market has been flooded with reports of staggering growth and blockbuster revenue figures, attracting a flood of developers and creating a number of “gold rush” success stories.

However, the market trend now appears to have quietly shifted direction: hit titles from major studios are dominating the charts for longer periods, while stories of underdogs achieving big wins are becoming increasingly rare. According to the data, the domestic mini-game market generated 53.535 billion yuan in revenue in 2025, representing a year-over-year growth rate of 34.39%. It remains the segment with the highest net value-added growth in the domestic gaming market, but its growth rate has slowed compared to the explosive growth seen in the previous two years.

At the same time, 70% of publicly listed gaming companies have made significant investments in this sector, with leading firms like Supercell entering the market with their full portfolio of titles. Blockbuster mobile games such as *Honor of Kings* and *Happy Match* have also launched mini-game versions, effectively raising the industry’s entry barriers to the level of native apps.

With growth slowing and competition intensifying on one hand, and industry giants crowding the market and raising the bar on the other, what is the current state of the mini-games market? Is the mini-games sector headed for a brutal survival of the fittest scenario by 2026?

01

Platform: "Two Giants + Diversification" Development

When discussing mini-games, we naturally have to start with the platforms. Mini-games have taken root and flourished on these platforms, and the unique characteristics of each platform’s ecosystem have shaped them into distinct forms.

WeChat Mini Games remains the largest platform for mini-games in China. Building on the foundation of WeChat, the nation’s most popular social media app, WeChat Mini Games has witnessed and driven the growth of the mini-game market through early strategic planning and strong support, making it a key battleground for a large number of developers.

Today, there are over 400,000 WeChat Mini-Game developers, including more than 300 teams that generate over 10 million yuan in quarterly revenue. Monthly active users have also surpassed 500 million, and playing mini-games on WeChat has become a daily habit for an increasing number of players. In 2025, user online time increased by 10% year-over-year compared to 2024, and the cross-month retention rate for core users reached as high as 90%.

In terms of products, WeChat Mini Games have achieved significant success in the hardcore gaming segment. Currently, a number of titles—including SLGs, RPGs, and card games—that rely on long-term operation have seen steady growth on the platform. Furthermore, as the trend toward hybrid gameplay continues to evolve, top-grossing games often conceal a hardcore progression-driven core beneath their casual aesthetics.

The growth of Douyin mini-games has been particularly remarkable in recent years. Last year (2025), revenue from Douyin mini-games surged by 100%, while the number of active users jumped by 120% year-over-year. The 7-day retention rate and average playtime per user both increased by approximately 20%, and the number of monetizing developers and products doubled. Notably, more than 10 new games achieved monthly revenue exceeding 10 million yuan.However, in terms of genres, casual and puzzle games remain the most popular on the Douyin platform.

Leveraging its natural short-video ecosystem, Douyin has also demonstrated a distinct advantage in "content distribution." During the operational phase, Douyin mini-games can attract player attention through trending short videos and live streams, driving conversions through entertaining content. It can be said that for Douyin mini-games, playability is the foundation, while "entertainment value" is the key factor determining their viral reach.Last year, Douyin launched more than ten mini-games by leveraging trending topics. Among them, over 20 new products generated more than 100 million topic views. At the same time, the proportion of revenue contributed by content-driven scenarios for mini-games increased significantly, reaching as high as 80% in certain RPG categories.

WeChat Mini Games and Douyin Mini Games, the two major platforms, are expected to account for more than 90% of the total revenue in China’s mini-game market, collectively defining the industry’s core base.

Beyond the "big two," other platforms such as Kuaishou, Alipay, and Meituan are still in a phase of building momentum. While their user bases and revenue shares remain relatively small, they are able to tap into niche user groups through differentiated use cases, generating incremental revenue for developers and even producing minor hits. According to reports, Alipay’s mini-game platform already produced a product with monthly revenue exceeding 100 million yuan last year, and there are more than 10 top-performing titles with monthly revenue exceeding 10 million yuan.

Alipay Mini-Games Top Charts

02

Manufacturers: A Clear Divide in Market Segments

At the same time, the explosive growth of the mini-game market has attracted a large number of game developers, ranging from well-established giants to small teams of just a few members. These teams have leveraged their respective strengths in the mini-game market to deliver a rich and diverse range of gaming experiences to players. However, as the market has evolved, it has inevitably seen a consolidation of the top players, and a significant trend of tiered differentiation has emerged among game developers.

The top tier is dominated by publicly traded companies or established game developers.

The explosive growth of the mini-game sector has attracted a large number of major players to the market; today, over 70% of publicly listed game companies have entered this space.Leveraging their robust R&D resources and exceptional operational capabilities, these companies have demonstrated overwhelming dominance in chart rankings and revenue generation through a strategy of “high-quality content combined with cross-platform operations.” They have also played a pivotal role in driving the quality upgrade of mini-games, with 37 Interactive Entertainment and DianDian Interactive serving as prime examples.

Backed by the company’s strategic focus and robust operational capabilities, 37 Interactive Entertainment has successively launched a string of blockbuster hits—including *Call Me the Grand Manager*, *Seeking the Way in the Vast Universe*, *The Unknowns*, *Time Explosion*, and *Heroes Without Flash*—each generating monthly revenue in the hundreds of millions. Thanks to its long-standing ability to keep multiple titles firmly at the top of the best-seller charts, it comes as no surprise that 37 Interactive Entertainment has once again successfully defended its position as the top company on this year’s list of the top 100 casual game companies.

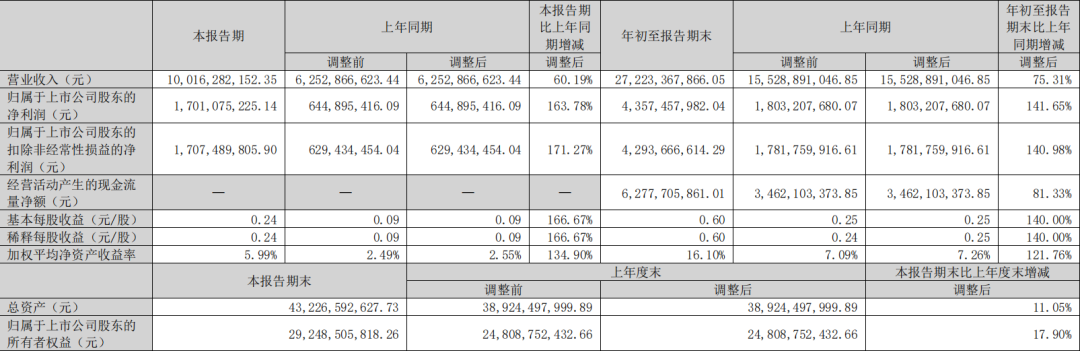

Dot Interactive, a subsidiary of Century Huatong, has created a “money-making legend” in the mini-games sector by adopting an “exclusivity and excellence” strategy and relying on just two core products: *Endless Winter* and *Bengbeng Kingdom*.These two products not only secured DianDian Interactive the second-place spot on the global mobile game publisher revenue rankings but also directly drove Century Huatong’s net profit to grow by 141.65% year-over-year in the first three quarters of 2025. The company’s market capitalization surpassed 100 billion yuan, marking a remarkable turnaround from its status as a “ST” stock to become the highest-valued gaming company on the A-share market.

Image source: Century Huatong’s Q3 2025 Financial Report

Established companies such as BoKe Technology, 4399, Online Tuyu, and Tanwan Games have also been expanding into the mini-games sector while continuing to focus on their traditional strengths, thereby creating a new and robust growth trajectory for themselves. Feiyu Technology, leveraging the success of its tower defense mini-game *One Step, Two Steps*, saw its revenue surge by 343.6% year-over-year in the first half of 2025, successfully turning a loss into a profit and achieving a remarkable turnaround in its performance.

The second tier consists of the leading companies in various market segments.

Most of these developers are “native teams” that have grown out of the casual gaming sector. With a deep understanding of the market’s underlying dynamics and user preferences, they are able to maintain an exceptionally high hit rate through precise insights into niche demands and rapid product iteration, making them the driving force behind innovation in the industry.

For example, Haoteng Jiake in Beijing has several mini-games with over 100 million monthly active users. Under the banner of “Crazy Games,” the company has reaped substantial commercial value and, through flagship titles such as *King of the Slacker* and *Crazy Knights*, pioneered two popular sub-genres—“Slacker-style” and “Loot Box-style”—becoming a benchmark that others in the industry are eager to emulate.

Haoteng Jiake's new game, *The Forsaken Land*, has begun its push for the top of the charts

With *Bullseye*, which generated hundreds of millions in revenue, *Dream Dragon Journey* single-handedly popularized the "Bullseye-style" concept. Riding this wave of popularity, the company went on to create *Shoot the Zombies*, a new hit that has consistently ranked in the top three on the best-seller charts;Since then, more titles such as *Defend the Sunflowers* and *Become a Lord* have consistently appeared on the charts, further solidifying the company’s strong position in the mini-game market.

The IAA sector has also seen the emergence of a number of highly representative teams: for example, Jianyou Technology, the developer behind *Sheep Sheep*, and Lanfei Interactive, the creator of *Catch the Goose*, have successfully broken into the mainstream thanks to their phenomenally popular hits; meanwhile, companies such as Zhise Network, Zhishang Technology, and Zunyue Network have deeply cultivated the user acquisition market, propelling numerous puzzle and brain-teaser games to success and establishing themselves as leading publishers in the IAA sector.

The phenomenal success of "Sheep Sheep" has made it a common belief that mini-games can generate tens of millions in daily revenue.

The third tier consists of small and medium-sized teams, which account for more than 70% of the total.

Given their limited R&D resources, weak risk-bearing capacity, and the competitive pressure from leading companies, such teams inevitably face greater challenges to their survival and growth. For them, the key to breaking through lies in two strategies: either partnering with leading publishers to leverage their momentum and break through the competition, or focusing on creativity to be the first to enter underdeveloped niche markets, thereby carving out a path to survival through differentiation.

A prime example of this is Linbei Interactive, a fledgling team of fewer than ten people. By tailoring its offerings to the preferences of female gamers and innovating with a marketing strategy that offers “real flowers for playing the game”—in addition to standard simulation gameplay—the team successfully propelled its title *My Garden World* into the top five of the best-seller charts as a dark horse.

03

Competition: A Multi-Dimensional Upgrade

It is clear from the distinct tiering of developers that competition in the domestic mini-games market has clearly entered a new phase.

The days when a small team and a budget of a few hundred thousand yuan could generate tens of millions in revenue—the era of grassroots gold rushes—are long gone; the unscrupulous tactics of making a quick buck with one-hit wonders have been rejected by the market.Today’s players are demanding “native app-level” quality from mini-games, and as the market leaders begin to solidify their positions, it has become increasingly difficult for new titles to break through. Influenced by these factors, competition in the industry has evolved from a simple battle for traffic into a comprehensive contest of “product quality + traffic acquisition + long-term operations + technical capabilities.”

At the product level, mini-game mechanics are evolving toward greater diversity and integration: on the one hand, wrapping hardcore games in a casual package and adding progression systems to casual games has become a common strategy for balancing user acquisition and monetization; on the other hand, amid a severe trend toward homogenization, selecting and re-integrating different core mechanics has also become a strategy for developers to achieve differentiated innovation.

At the same time, the quality of mini-games has already made significant strides. With the support of constantly improving underlying technologies, a smooth and seamless gaming experience has become the basic standard for these products, making it possible for mini-games to come very close to matching the quality of native mobile games.

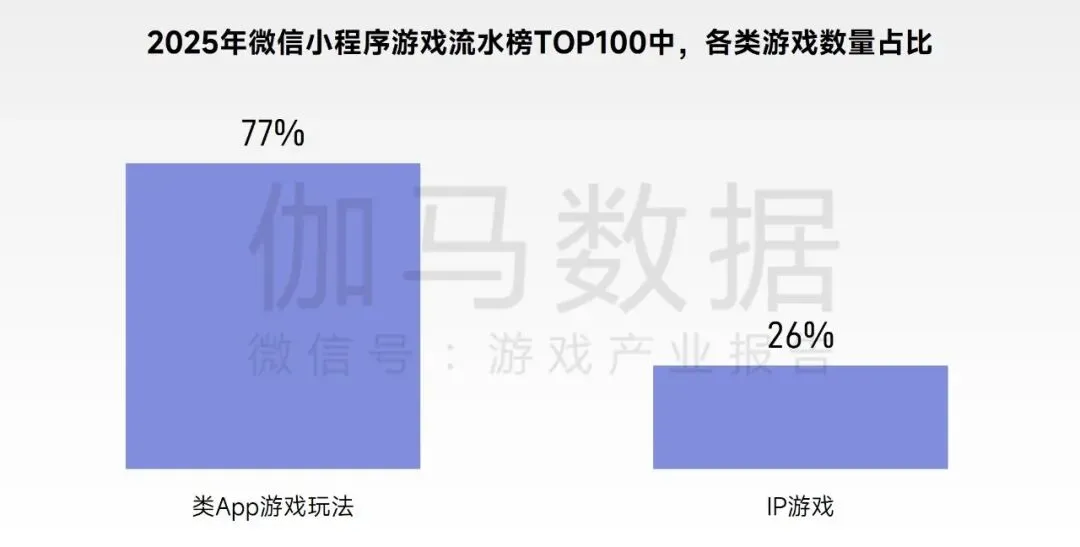

App-like products and IP adaptations have become the main drivers of growth in mini-games

In terms of traffic, acquisition costs are rising daily, and the industry’s focus is gradually shifting from conventional user acquisition to omnichannel content marketing. Emerging channels such as live streaming and short videos have become new battlegrounds for traffic acquisition. Notably, the paid activation rate for live streaming is 108% higher than that of short videos, making it a new engine driving growth.At the same time, two emerging traffic hubs—PC platforms and Video Accounts—have demonstrated immense potential. The active user base for PC mini-games grew by 55% year-over-year this year, with commercial revenue increasing by 40% and ad spending on user acquisition surging by 400%.

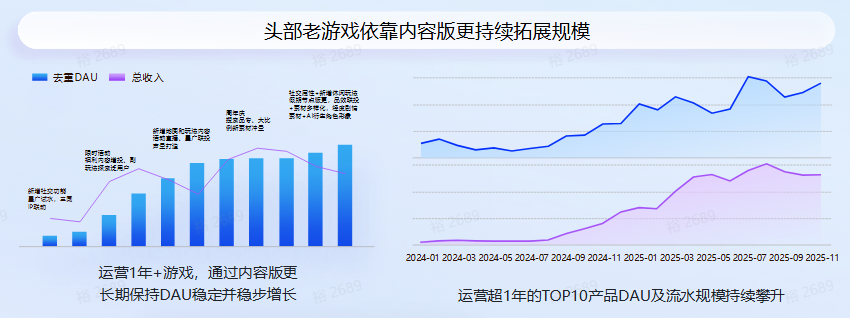

From an operational perspective, long-term operation has become the industry standard. Data shows that during content updates, the activation rate of new materials can increase by 20%, and the return rate can grow sixfold; as a result, many leading products maintain user engagement through frequent updates. In addition, seasonal designs and regular IP collaborations are becoming standard features for an increasing number of mini-game products.

From a technical perspective, AI is already capable of comprehensively empowering the development, launch, and monetization of mini-games, and is becoming a key barrier for developers to build core competitiveness. The impact of AI is particularly significant during the product launch phase.The head of 37 Interactive Entertainment’s AILab has noted that AI-generated 2D art assets now account for over 80% of the company’s publishing materials, while 3D assets exceed 30%. AI-driven advertising campaigns make up 50% of the company’s efforts, boosting efficiency by 70%. Furthermore, AI-powered customer service has been rolled out across all of the company’s games, with a response accuracy rate exceeding 80%.

Conclusion

Although "mini-games" are a common format worldwide, China's mini-games today stand in a league of their own in terms of scale, integration with platform ecosystems, and commercial maturity.

From its early days of ad overload, shoddy production, and limited gameplay variety to today’s refined rules, diverse categories, and mature commercial ecosystem, the domestic mini-game market’s remarkable transformation is the result of platforms’ long-term dedication and developers’ meticulous efforts.

The current slowdown in market growth does not signal the end of the boom; rather, it represents an inevitable shift in the mini-games industry from “unregulated expansion” to “careful cultivation.” This means that future opportunities will no longer belong to speculators jumping on the bandwagon, but will instead favor long-term thinkers who accurately understand platform characteristics, dedicate themselves to refining high-quality content, and master core technologies.

The casual gaming industry will eventually shed its restlessness during this transition from "speed" to "stamina," fostering a more vibrant ecosystem and moving toward a new phase of high-quality development.

原创文章,作者:游茶妹儿,禁止转载:https://youxichaguan.com/en/archives/195264